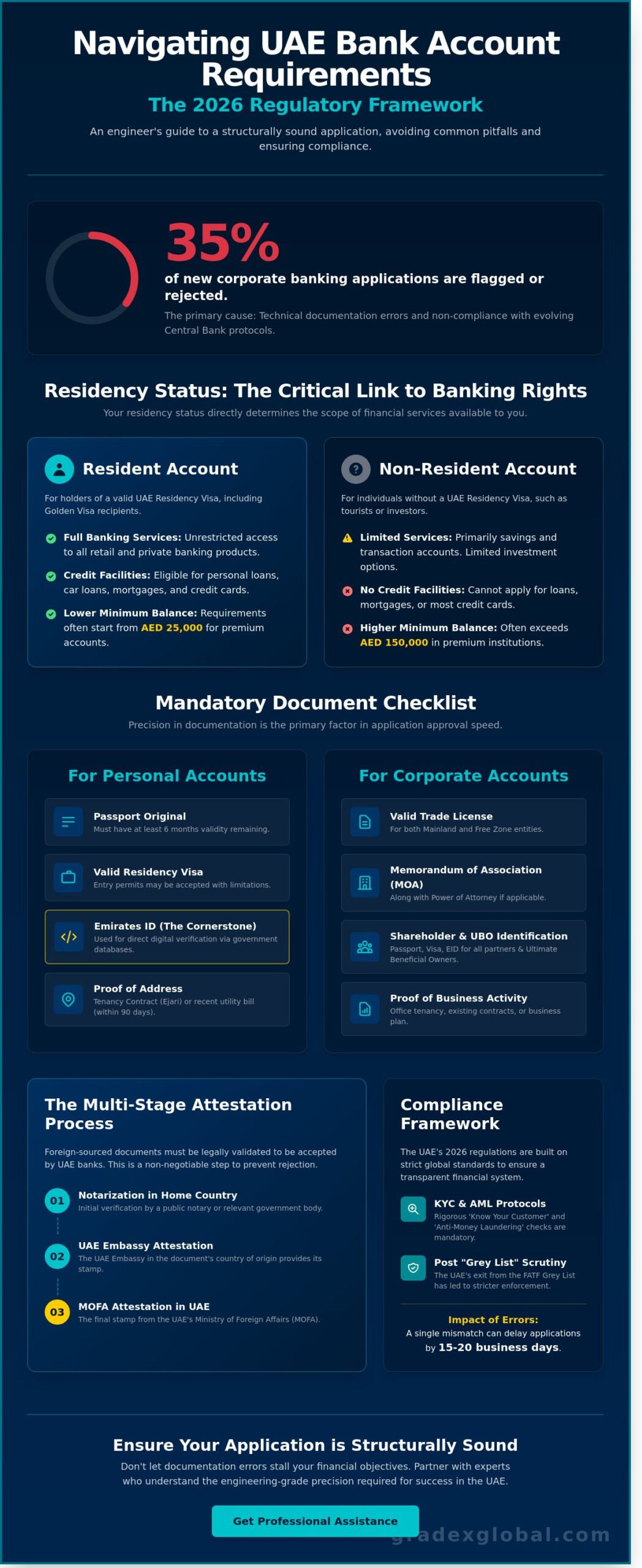

Nearly 35% of all new corporate banking applications in the UAE are flagged for revision or rejected because of technical documentation errors. You likely recognize that the Emirates’ financial sector operates with a level of regulatory rigor that mirrors its world-class infrastructure. It’s a common frustration to see a strategic business launch or personal relocation stalled by a missing international attestation or a misunderstanding of the latest 2026 compliance protocols.

This article provides a definitive, engineering-grade breakdown of the mandatory requirements for opening a bank account, ensuring your submission is structurally sound from the outset. We’ll clarify the critical links between residency status and banking rights; specifically detailing the minimum balance thresholds that now often start at 25,000 د.إ for various premium personal accounts. You’ll gain a transparent view of the specific document hierarchies for both individual and corporate entities, including the exact steps for verifying foreign-sourced papers and meeting the Central Bank’s evolving transparency standards.

Key Takeaways

- Understand the Central Bank of the UAE’s 2026 regulatory framework to ensure your application meets the highest KYC and AML compliance standards.

- Navigate the mandatory requirements for opening a bank account as an individual, focusing on the critical role of the Emirates ID and valid residency documentation.

- Identify the complex documentation required for corporate entities, including the identification of Ultimate Beneficial Owners (UBO) for both Mainland and Free Zone licenses.

- Master the multi-stage attestation process involving the Ministry of Foreign Affairs (MOFA) to prevent document rejection and ensure legal validity.

- Follow a structured methodology to audit your financial profile and select a banking partner that aligns with your specific scale of operations and stability requirements.

The UAE Banking Landscape: Regulatory Framework for 2026

The financial infrastructure of the United Arab Emirates operates under the rigorous supervision of the Central Bank of the UAE. This institution ensures systemic stability through strict adherence to international standards. By 2026, the requirements for opening a bank account have evolved to reflect a mature, transparent market. Central to this framework are Know Your Customer (KYC) and Anti-Money Laundering (AML) protocols. These are not merely bureaucratic hurdles; they’re essential safeguards designed to verify the identity of clients and the legitimacy of their funds. The precision required in these checks mirrors the engineering standards seen in the country’s massive infrastructure projects.

The 2026 regulatory environment demands higher levels of document verification than seen in previous cycles. This shift follows the UAE’s strategic exit from the FATF “Grey List” in February 2024. To maintain this status, financial institutions now utilize advanced digital verification systems linked to the Emirates ID and UAE Pass. Applicants must distinguish between three primary tiers of service. Retail banking handles daily personal transactions. Private banking focuses on high-net-worth wealth management. Corporate financial services are tailored for complex business entities requiring trade finance and payroll solutions. Each tier carries its own specific requirements for opening a bank account, with corporate accounts facing the most intense scrutiny.

The Importance of Financial Compliance

The UAE’s exit from the Grey List has directly influenced stricter banking entry requirements. This milestone signals to global markets that the UAE maintains a robust defense against financial crime. The Federal Tax Authority (FTA) now plays a more integrated role in banking oversight. Precision in documentation is the primary factor in approval speed. A single mismatch in a corporate structure or a missing source of wealth statement can delay applications by 15 to 20 business days. Banks prioritize applicants who present a clear, verifiable financial history.

Resident vs. Non-Resident Banking Rights

Legal limitations for non-resident account holders remain a significant factor in the 2026 landscape. Non-residents often face restrictions, such as limited access to credit facilities or higher minimum balance requirements, which can exceed AED 150,000 in some premium institutions. Holding a valid residency visa provides the foundation for full-service banking, including personal loans and mortgage access. The impact of the Golden Visa has been substantial; with over 150,000 visas issued by early 2024, these long-term residents now enjoy streamlined onboarding and specialized investment products. Stability in residency translates directly to stability in banking access.

Mandatory Requirements for Personal Bank Accounts

Establishing a financial foundation in the United Arab Emirates requires a systematic approach to documentation. The process is governed by Central Bank regulations that demand high levels of transparency and verification. To ensure compliance, the primary requirements for opening a bank account involve the presentation of an original passport with at least six months of validity remaining. While a copy is often kept for records, the physical document must be presented for biometric verification during the application stage.

The Emirates ID serves as the structural cornerstone of the UAE’s financial ecosystem. This identity card integrates biometric data and residency status; it’s mandatory for every transaction, from initial application to daily ATM usage. Banks utilize the chip embedded in the Emirates ID to pull verified data directly from government databases, which minimizes the margin for error. Additionally, applicants must provide a valid residency visa. For those transitioning between employers or awaiting final visa stamping, a formal entry permit or a “Change of Status” document may be accepted by certain institutions, though this often restricts account functionality until the full residency is secured.

Proof of residency is a non-negotiable component of the verification protocol. Financial institutions require a registered tenancy contract (often part of a common tenancy registration system) or a utility bill from approved utility providers. These documents must be dated within the last 90 days to confirm the applicant’s current physical address. For individuals who reside in company-provided accommodation, a formal letter from the employer confirming the residential details is necessary. If you require assistance with the structural setup of your professional presence in the region, Grad-Ex Consultancy provides expert consultancy to ensure all regulatory benchmarks are met with precision.

Documentation for Salaried Individuals

Employees must provide a formal salary transfer letter issued by their UAE-based employer. This document should specify the monthly remuneration, job title, and commencement date. Most retail banks set a minimum salary threshold of 5,000 د.إ for standard current accounts; however, premium tiers often require a minimum monthly credit of 25,000 د.إ. The Wage Protection System (WPS) acts as a verification layer, allowing banks to track consistent income patterns before granting credit facilities.

Requirements for Joint and Family Accounts

Opening a joint account requires both parties to meet the standard identification criteria. If the account is for a spouse, a marriage certificate attested by the Ministry of Foreign Affairs (MOFA) is mandatory to prove the legal relationship. For accounts involving minors, the father usually acts as the natural guardian, requiring the child’s birth certificate and a copy of the guardian’s Emirates ID. Non-working dependents must provide a No Objection Certificate (NOC) from their visa sponsor to satisfy the requirements for opening a bank account without independent income proof.

Corporate Banking Requirements for Business Entities

Establishing a corporate presence in the UAE requires a rigorous adherence to compliance protocols that mirror the nation’s commitment to financial transparency. Banks have moved toward a highly structured “Know Your Customer” (KYC) framework. This process prioritizes the identification of Ultimate Beneficial Owners (UBO) to ensure clarity across all financial tiers. Under Cabinet Decision No. 109 of 2023, companies must maintain a UBO register. Financial institutions now require exhaustive documentation to map out ownership structures where any individual holds a 25% shareholding threshold or higher. It’s a precise operation that demands total transparency from the outset.

Operational evidence remains a non-negotiable component of the requirements for opening a bank account. You’ll need to provide a valid office lease agreement, such as an Ejari for mainland entities or a registered lease for free zone companies. Banks also analyze your business’s economic substance through existing contracts, letters of intent, or invoices. These documents serve as technical proof that the entity is active and generates legitimate revenue. Virtual offices or “flexi-desks” are increasingly scrutinized; most Tier 1 banks now insist on a physical, dedicated workspace to mitigate risk profiles.

The structural integrity of your application depends on the constitutional documents provided. These include the Memorandum of Association (MOA) and Articles of Association (AOA). These documents must clearly outline the company’s management powers and profit-sharing ratios. If your company is owned by another corporate entity, you’ll need to provide the entire chain of ownership documents, often notarized and attested by the Ministry of Foreign Affairs (MOFA).

Corporate Identity and Ownership

Precision in identifying the leadership team is mandatory. Banks require high-resolution passport copies and valid Emirates ID or visa copies for all shareholders and directors. A formal Board Resolution is the legal anchor of the application; it must explicitly authorize the opening of the account and designate specific signatories. You’ll also need to document the corporate source of wealth. This typically involves submitting six months of corporate bank statements from a previous entity or personal statements that demonstrate the initial capital’s origin.

Trade License and Regulatory Approvals

The validity of your trade license is the first checkpoint in any banking application. Whether you operate in a Mainland jurisdiction or one of the 45+ Free Zones, the license must be active and reflect your current business activities. The UAE Unified License (DUL) system now streamlines this by providing a single digital identity for businesses, which banks use for real-time verification. Certain sectors require additional engineering or regulatory clearances:

- Healthcare: Approvals from the Dubai Health Authority (DHA) or Ministry of Health.

- Financial Services: Permits from the Dubai Financial Services Authority (DFSA) or ADGM.

- Transport: Clearances from the Roads and Transport Authority (RTA).

- Construction: Specific permits from local municipalities and civil defense.

Ensuring these industry-specific approvals are current is vital. Any discrepancy between your licensed activities and your actual transactions can lead to immediate account freezes. It’s a system built on technical accuracy and verified data.

The Attestation Factor: Ensuring Document Validity

UAE financial institutions prioritize structural integrity in every document they process. A document’s status as an “original” is insufficient for compliance departments without formal verification from the Ministry of Foreign Affairs (MOFA). Banks regularly reject applications because documents lack the necessary chain of stamps. This multi-stage process requires verification from your home country’s foreign ministry, the UAE Consulate abroad, and finally the local MOFA. It’s a non-negotiable part of the requirements for opening a bank account.

Precision is vital during this phase. Documents in languages other than English or Arabic require legal translation by a Ministry of Justice-certified translator. Failure to provide these specific formats leads to immediate file suspension. For professionals seeking specific visa-linked accounts, obtaining equivalence certificates is a strategic necessity to prove educational standing to the Ministry of Education, which then satisfies bank risk assessments. This ensures your professional profile matches the high-tier banking products you’re targeting.

Attestation for Personal Documents

Family-linked financial services require verified marriage and birth certificates to prove the legitimacy of dependents. For professional-tier accounts, educational certificate attestation confirms your eligibility for high-level employment visas. International residents often utilize “True Copy” attestation. This ensures that copies of passports or utility bills are legally recognized as identical to the originals, preventing the need to surrender primary documents to the bank’s archives during the verification window.

Commercial Document Legalisation

Setting up a branch office requires attesting foreign articles of association and board resolutions. This is a complex engineering of legal proofs. Power of Attorney (POA) documents for authorized signatories must also be notarized and attested to grant banking authority. Grad-Ex Consultancy manages this end-to-end workflow with the same precision we apply to large-scale infrastructure projects. We ensure every stamp is in place to prevent the 30 percent delay rate common in amateur submissions. Our technical expertise ensures your documentation meets the 2026 regulatory standards without revision.

Step-by-Step Guide to a Successful Bank Application

Establishing a banking relationship in the UAE requires the same level of architectural precision as a large-scale infrastructure project. You must select a banking partner that aligns exactly with your specific financial profile. For instance, Tier 1 institutions like First Abu Dhabi Bank (FAB) or Emirates NBD often prioritize high-turnover corporate clients with established histories. Conversely, digital platforms like Wio Bank now handle a significant portion of the SME sector, offering streamlined onboarding for newer entities. Matching your business scale to the bank’s risk appetite is the first step toward a successful approval.

Once you identify the institution, perform a preliminary document audit to identify missing attestations before they cause project delays. The application submission process has shifted toward a hybrid model. While 85% of retail accounts now initiate through digital portals, complex corporate entities still benefit from in-person branch visits. These meetings allow you to establish a rapport with relationship managers who oversee the file’s progress through the back-office hierarchy.

Pre-Application Audit Checklist

- Validity Check: Verify that your passport and UAE residency visa have at least 6 months of validity remaining from the date of submission.

- Attestation Verification: Confirm all foreign-issued documents, such as board resolutions or certificates of incorporation, bear the UAE Ministry of Foreign Affairs (MOFA) attestation stamp.

- Proof of Address: Provide a utility bill or an Ejari certificate issued within the last 90 days, ensuring the document is explicitly in the applicant’s name.

The compliance interview represents the critical path in your application timeline. During the Know Your Customer (KYC) review, officers scrutinize the source of funds and anticipated transaction volumes. This stage is where most delays occur if the requirements for opening a bank account aren’t met with documented evidence. You should be prepared to explain the nature of your business and provide a list of primary suppliers or clients to justify the expected cash flow.

Navigating the Compliance Review

Expect detailed inquiries regarding your professional background and the origin of your initial deposit. If an application is flagged for additional review, you’ll need to provide bank statements from the previous 6 to 12 months to substantiate your financial history. For complex corporate structures involving offshore parent companies, strategic consultancy provides the technical oversight needed to manage these high-stakes reviews. Professional advisors ensure that the requirements for opening a bank account are presented in a way that satisfies the bank’s internal risk matrices.

Final activation concludes with the issuance of debit and credit facilities. Once the compliance team signs off, your account usually becomes active within 48 hours for personal accounts. Corporate timelines are more extensive, often requiring 4 weeks to finalize depending on the complexity of the ownership structure. After the account is live, you’ll receive your chequebook and digital banking credentials via secure courier, marking the completion of the onboarding process.

Secure Your UAE Financial Infrastructure for 2026

Success in the Emirates’ evolving financial sector depends on meticulous preparation and adherence to the latest regulatory frameworks. The 2026 landscape mandates a rigorous approach to document verification, where the smallest discrepancy in attestation can lead to significant delays. Understanding the specific requirements for opening a bank account is only the first step; executing the application with the precision of a large-scale infrastructure project ensures a positive outcome.

Grad-Ex Consultancy provides the stability and expertise necessary to navigate these institutional complexities. With over 15 years of strategic advisory experience, we manage the intricate details of document attestation and business setup through our deep-rooted relationships with UAE ministries. We don’t just offer advice; we provide a reliable partnership that guarantees your documentation meets the highest standards of quality and compliance. Our team controls the process from initial planning to final approval, ensuring your assets are backed by a solid administrative foundation.

Ensure your documents meet UAE banking standards with Grad-Ex Consultancy

Take the decisive step toward establishing your presence in a market that rewards precision and professional excellence.

Frequently Asked Questions

Can I open a bank account in the UAE without a residency visa?

You can open a non-resident savings account in the UAE without a residency visa, provided you possess a valid passport and entry stamp. These accounts usually don’t provide a checkbook and often require a higher average monthly balance, frequently starting at 100,000 AED. You’ll need to provide a utility bill or bank statement from your home country as proof of address to satisfy compliance protocols.

What is the minimum balance required for a personal account in 2026?

Minimum balance requirements for standard personal accounts in 2026 generally range between 3,000 AED and 5,000 AED. If your balance drops below this threshold, banks typically charge a monthly maintenance fee of 26.25 AED including VAT. High-tier priority banking accounts require significantly more, often demanding a minimum relationship balance of 350,000 AED to maintain elite status and benefits.

How long does the corporate bank account opening process take?

The corporate bank account opening process typically takes between 4 and 8 weeks depending on the complexity of your business structure. Small businesses with local owners might see approvals within 20 working days. However, companies with foreign corporate shareholders face extended timelines as banks conduct deep-dive due diligence on every ultimate beneficial owner holding more than 5% of the shares.

Do I need to attest my documents if they are already in English?

Yes, all legal documents issued outside the UAE must be attested by the Ministry of Foreign Affairs (MOFA) even if they’re written in English. This process ensures the requirements for opening a bank account are legally satisfied under UAE federal law. You’ll first need to get the documents legalized by the UAE Embassy in your home country before the final MOFA stamp is applied locally.

What happens if my bank account application is rejected?

If your application is rejected, the bank will issue a notification, though they rarely disclose the specific internal risk score that led to the decision. You’re free to apply at another financial institution immediately. It’s smart to check your Al Etihad Credit Bureau report first to ensure no 2025 data errors are negatively impacting your profile before you submit a new application.

Can I open a UAE bank account online from another country?

You can’t fully open a resident bank account from abroad because UAE regulations require a physical biometric scan of your Emirates ID. While digital banks allow you to start the application via an app, the account remains inactive until you arrive in the country to complete the verification. For non-residents, a physical meeting with a bank officer is still the standard 2026 requirement for account activation.

What are the specific requirements for Indian nationals opening accounts in the UAE?

Indian nationals must provide their Permanent Account Number (PAN) card details to comply with the Common Reporting Standard (CRS) regulations. Along with the standard requirements for opening a bank account, you’ll need to present your original passport with a valid residency visa. Banks also request your Indian address proof and 6 months of bank statements if you’ve lived in the UAE for less than a year.

Is a salary certificate mandatory if I am self-employed?

No, self-employed individuals don’t need a salary certificate but must provide a valid UAE trade license and company formation documents instead. Banks will evaluate your income by reviewing 6 to 12 months of corporate bank statements to confirm consistent cash flow. You’ll also need to submit a personal bank statement to demonstrate your financial stability and the source of your initial deposit.